Blake

Thank you for clarifying—it’s great that you're thinking proactively and documenting the loan properly. Lending money to your own single-member LLC can be an effective way to capitalize the business while preserving legal clarity, but there are indeed several important legal considerations to keep in mind. I’ll walk you through the key points:

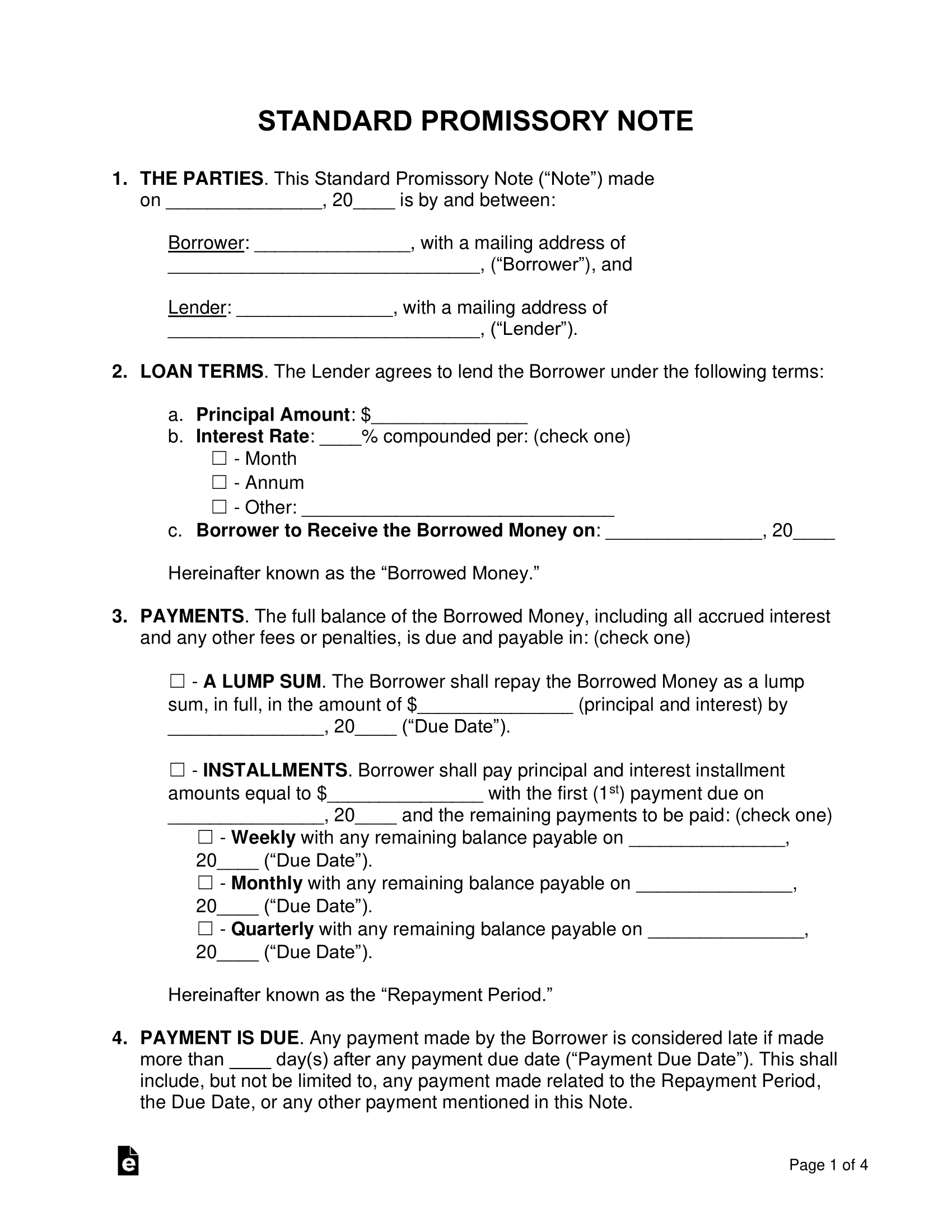

1. Formal Loan Documentation Is Essential

You're absolutely correct to prepare a formal loan agreement. Even though you're lending to your own LLC, it's vital to treat the transaction as if it were between unrelated parties. This helps preserve the corporate veil and avoid any appearance of commingling personal and business assets. The loan agreement should include:

- Principal amount

- Interest rate (ensure it complies with Utah's usury laws)

- Repayment schedule

- Maturity date

- Late payment terms (if any)

- Any collateral or security interest (if applicable)

2. Maintain Proper Records

Ensure that both the loan and its repayment are clearly reflected in the LLC’s books and bank accounts. Record the liability in your accounting software and avoid using business funds for personal expenses unless properly accounted for.

3. Interest and Tax Implications

Even though it's your own company, the IRS requires that interest be charged at a market rate, otherwise it could recharacterize the transaction. The interest you receive as the lender is taxable income, and the LLC may be able to deduct it (depending on how it uses the funds).

4. Respect the LLC’s Separate Legal Identity

Even as a single-member LLC, the business is a separate legal entity. Be sure to execute the agreement between yourself as an individual and in your capacity as the LLC manager. Sign both sides of the agreement accordingly, using your title to reflect the different roles.

5. Banking and Fund Transfers

Use separate bank accounts and transfer the loan funds from your personal account to the LLC's account with a clear memo indicating it is a loan. Avoid using personal credit cards for business expenses without documentation.

6. Default Terms and Remedies

Even though you control both sides, include language on what happens in the event of default. This is important for maintaining the enforceability of the agreement, and may also be relevant in the event of bankruptcy or future audits.

7. Future Investors or Creditors

If your LLC ever seeks outside financing or investment, having a formal loan agreement in place shows professionalism and avoids questions about unrecorded owner contributions or withdrawals.

8. Utah-Specific Legal Compliance

Utah law does not prohibit members from lending to their LLCs, but the interest rate you charge must not exceed the state’s maximum allowable interest rate (the legal limit is typically 10% if not specified in a written agreement). You’ll want to review Utah Code § 15-1-1 (Utah Code § 15-1-1) to ensure compliance.

You are absolutely on the right path by thinking through this and creating a written loan agreement. If you want a template tailored to Utah law, or assistance drafting a fully enforceable document, I strongly recommend hiring a local business attorney. You can find qualified Utah-based attorneys at www.avvo.com.

Does this answer your question and do you understand the answer completely? Please let me know if you have any follow-up questions or if anything in this answer was unclear, and I will be happy to help.

14

14

4

4

Solved

Solved

Create Document

Create Document